November 2024 Monthly Market Insights

Data and opinions as of October 31, 2024

Anticipation mounts as election volatility sends ripples through markets

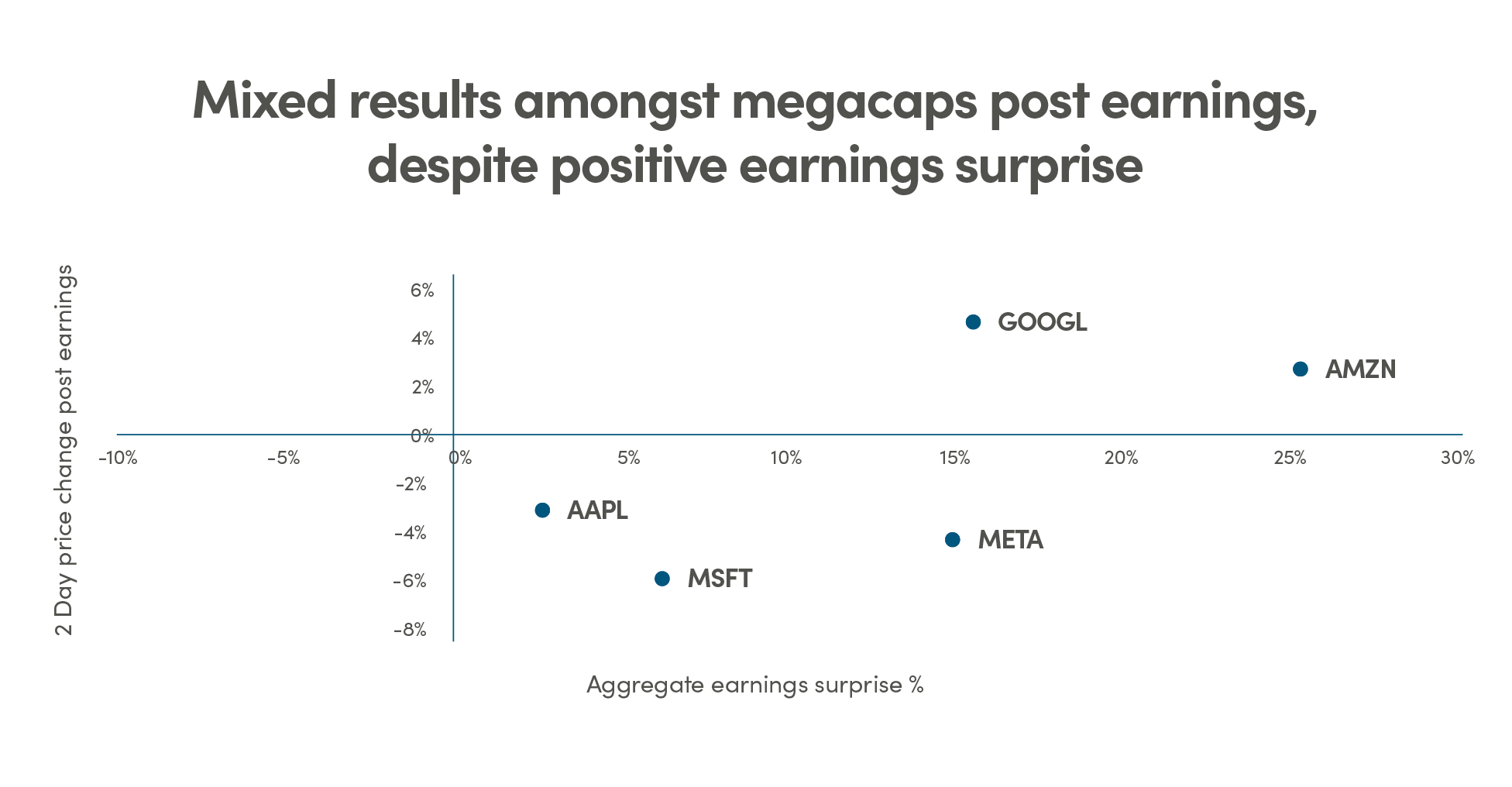

In October 2024, five of the "Magnificent 7" tech stocks—Alphabet, Microsoft, Meta Platforms, Amazon, and Apple—reported their earnings, capturing significant investor attention amidst the volatility ahead of the 2024 U.S. Election. Compounding this uncertainty, U.S. Treasury yields surged and the dollar strengthened, reflecting heightened expectations surrounding the upcoming elections as investors navigate these turbulent conditions heading into 2025.

NEI perspectives

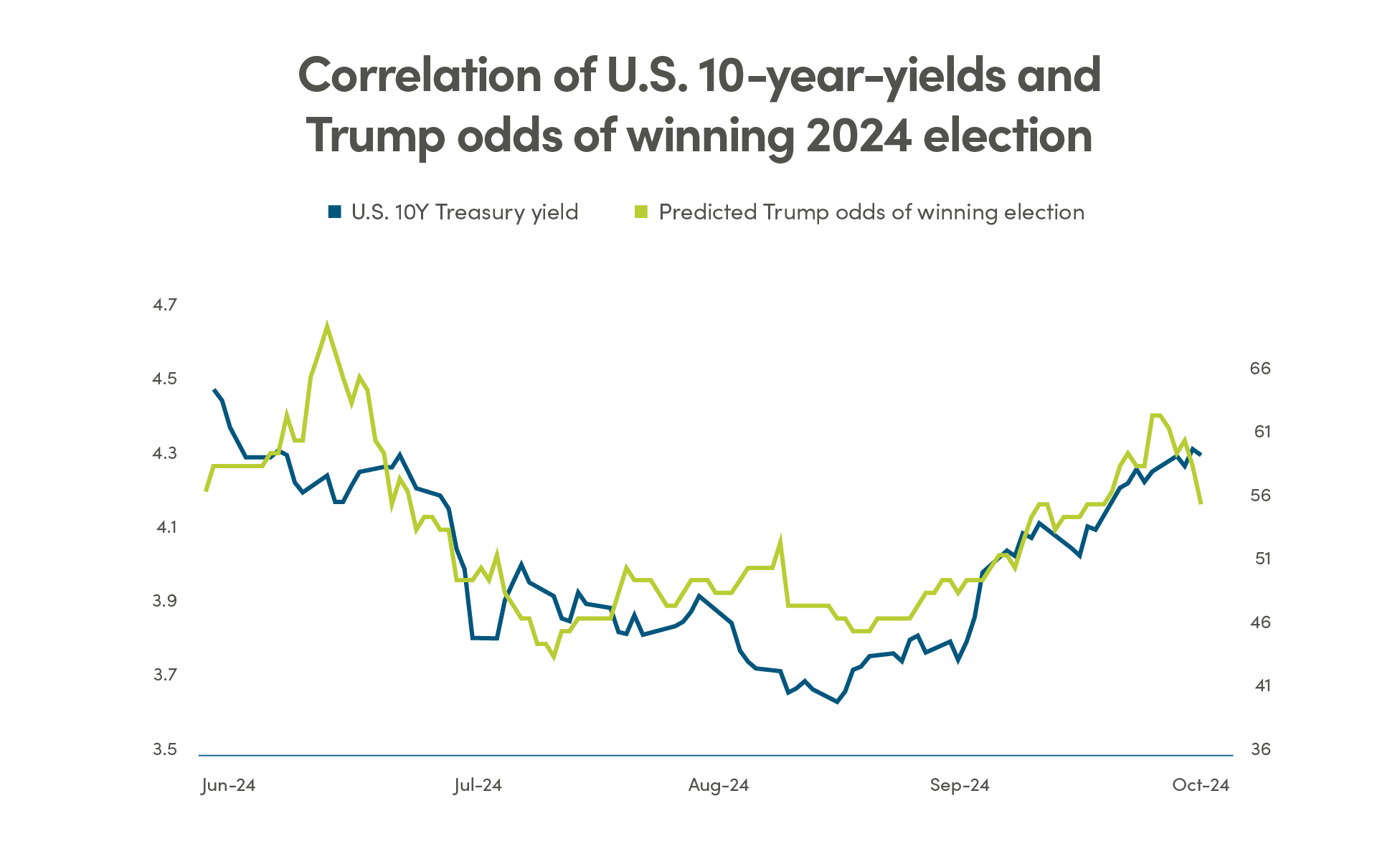

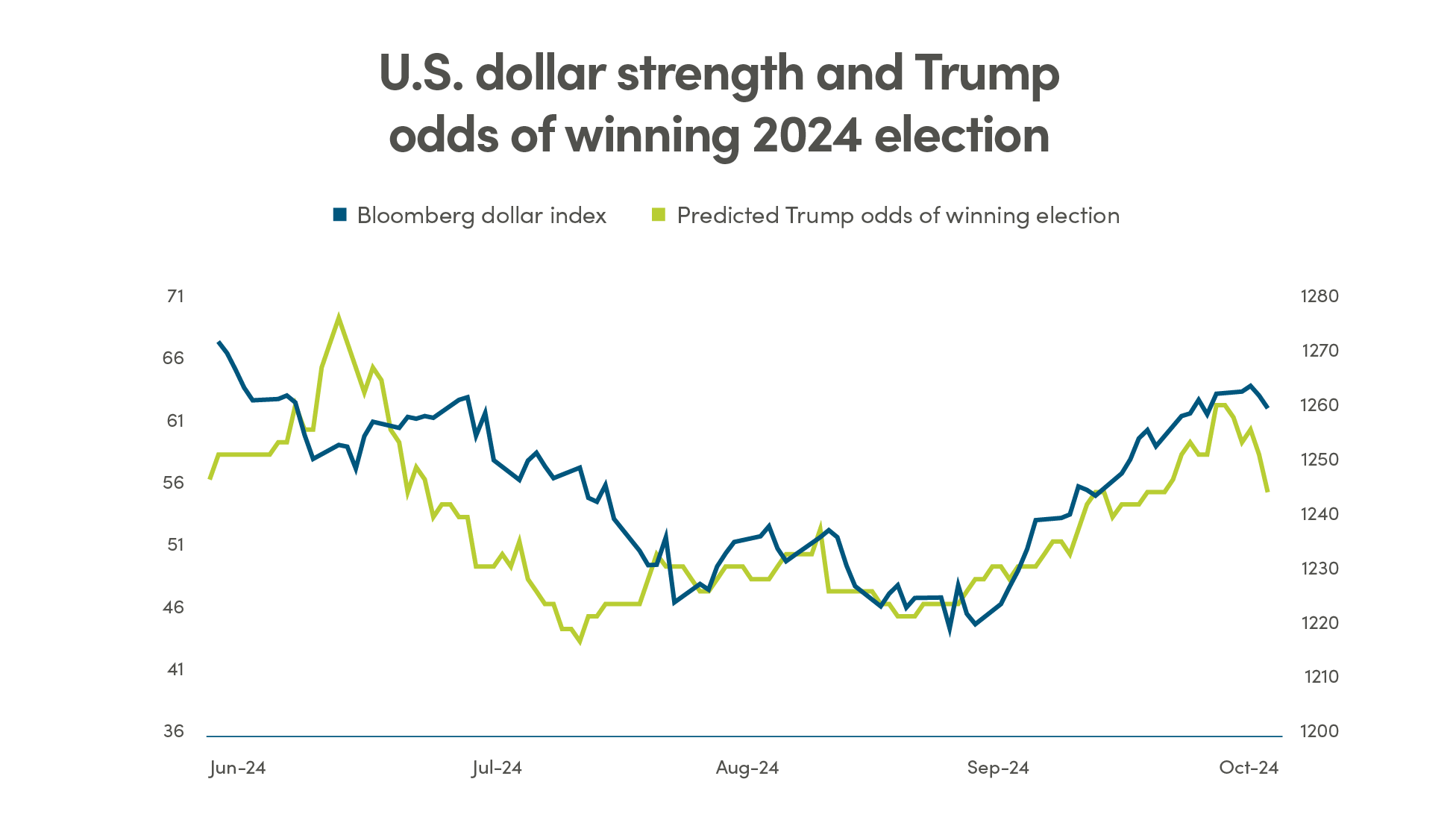

U.S. Treasury yields rallied sharply alongside a strengthening dollar and renewed interest in the "Trump trade," reflecting Trump’s rising odds according to polls and heightened expectations of a Republican sweep in the upcoming election. At the time of writing, the tentative election results confirm this expectation, and hence the expectation of pro-business policies are boosting equity markets due to the proposed tax cuts while negatively impacting fixed income due to inflation risk posed by these policies. Bottom line: although political dynamics shaped market sentiment in the weeks leading up to the election, politics historically have little impact on market performance over the long term.

Earnings reports from five of the "Magnificent 7" tech stocks revealed strong overall performance but fell short of some analysts' high expectations for growth in key areas, leading to cautious market sentiment. Bottom line: while the results were positive, concerns about slowing growth in critical segments could signal vulnerabilities as investors navigate an uncertain economic landscape.

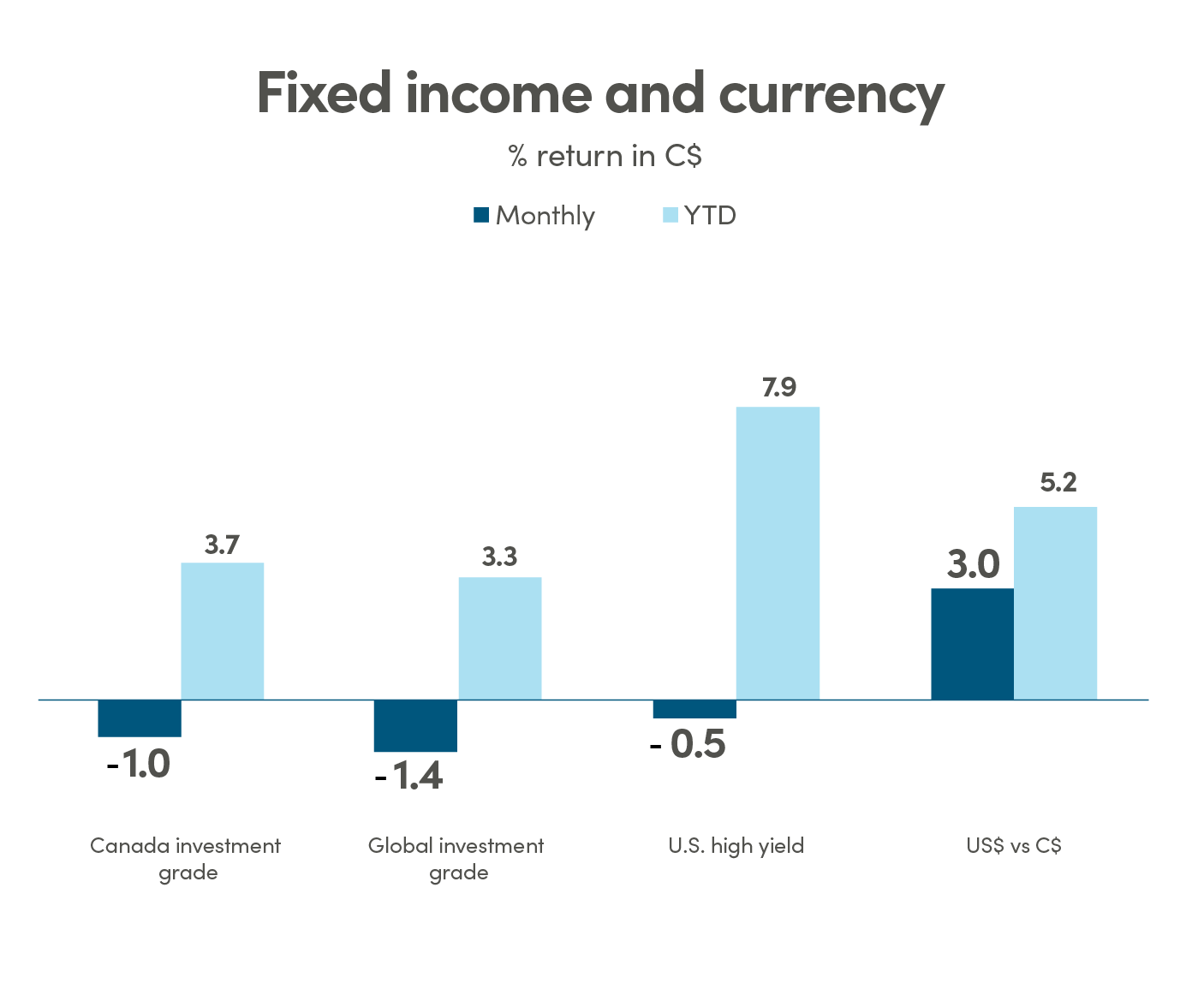

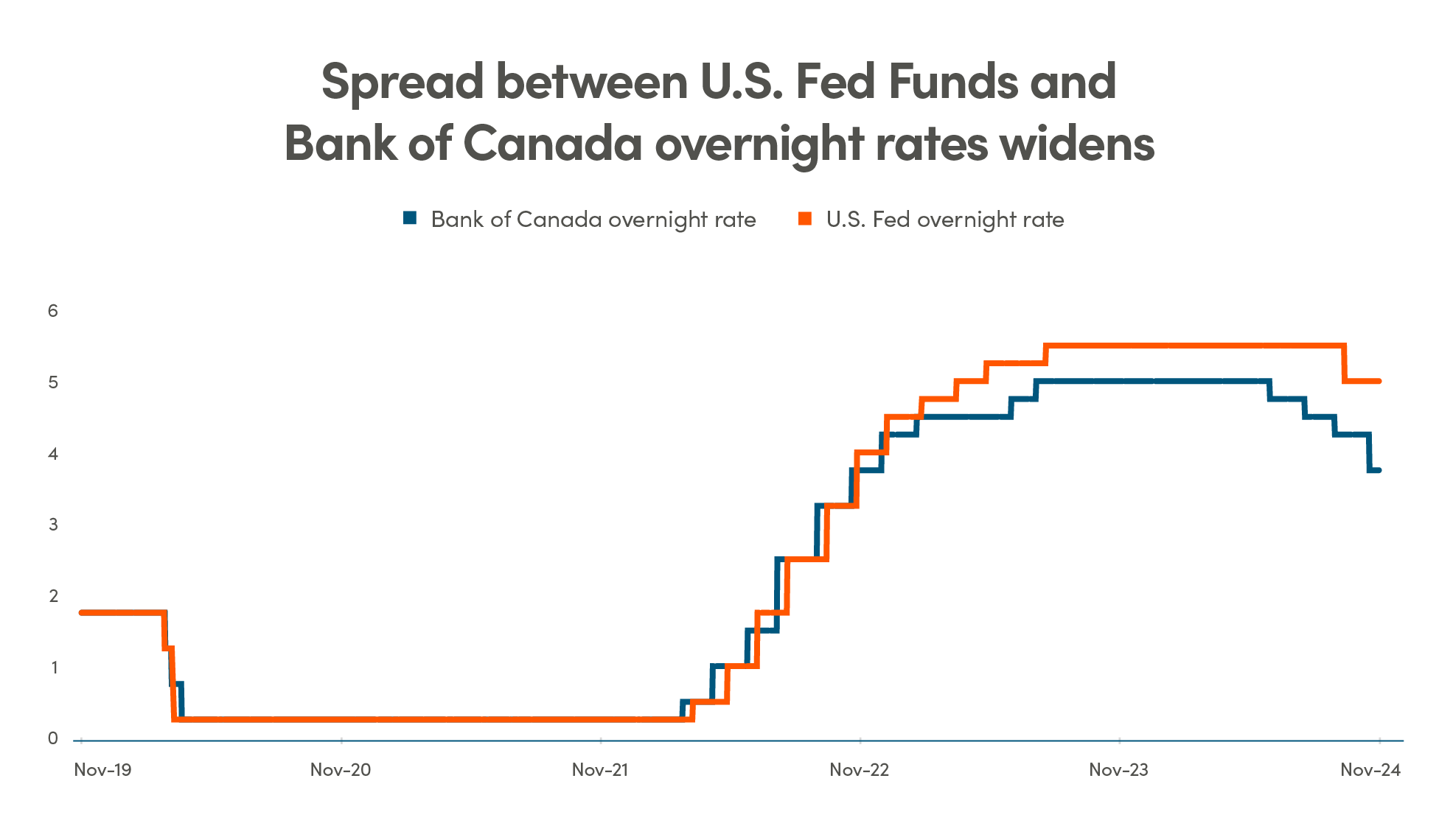

The divergence between Canadian and U.S. interest rates became increasingly pronounced, with the Bank of Canada cutting its key lending rate to 3.75%, resulting in a notable 125 basis point spread versus the U.S. Federal Reserve at 5.00%. The widening gap raises concerns about the potential for Canadian dollar to depreciate further, especially when economic outlook for Canada continues to be weaker relative to the growth in the U.S. Bottom line: as the interest rate landscape shifts, the significant spread between Canadian and U.S. rates will continue to affect currency valuations and economic expectations.

Canada: MSCI Canada; U.S.: MSCI USA; International: MSCI EAFE; Emerging markets: MSCI Emerging Markets. Source: Morningstar Direct

Canada investment grade: Bloomberg Barclays Canada Aggregate; Global investment grade: Bloomberg Barclays Global Aggregate; U.S. high yield: Bloomberg Barclays U.S. High Yield Index. Source: Morningstar Direct

Yields, U.S. dollar, Trump trade

In October 2024, U.S. Treasury yields, particularly the 10-year yield, experienced a sharp rally, rising by 77bps since September 16 to 4.38% on November 1, alongside the rise in the odds of a Trump win according to the polls. As the election results materialize in favor of a Republican Sweep, this surge has extended 10-year yields to +4.73%. This increase has been accompanied by a strengthening of the U.S. dollar and a resurgence in the so-called "Trump trade" equity basket - stocks that are expected to benefit from policies proposed by the Trump campaign. Fixed income assets took a negative hit when the yields rallied, as the proposed policies by the Trump campaign could lead to a resurgence of inflation and the market may need to pare back rate cut expectations. Policies proposed by Kamala Harris were expected to have minimal impact on inflation, hence having less impact on yields.

As markets have priced in a higher probability of a Republican sweep in Congress, there is an underlying optimism that such a scenario could foster an environment conducive to investment and growth. Looking ahead to 2025, if these trends continue, we may see an increased focus on sectors that align with Republican policies, alongside potential volatility as markets adjust to evolving fiscal and monetary landscapes.

Source: Bloomberg, NEI Investments

Magnificent 7 earnings

During the last week of October 2024, five of the "Magnificent Seven" stocks—Alphabet, Microsoft, Meta Platforms, Amazon, and Apple—reported Q3 earnings, drawing significant attention from investors. Analysts projected robust revenue growth across these tech giants, but the overall market response was cautious due to concerns about a potential slowdown in earnings growth coupled with elevated valuations. This quarter's expected average growth rate for these companies marked the slowest in six quarters, leading to increased scrutiny from market participants.

Source: Bloomberg, NEI Investments

The broader market reacted with volatility as investors questioned the sustainability of above-trend revenue and earnings growth, coupled with elevated valuations. The U.S. stock market had continuously hit all-time highs, driven largely by the largest AI and semiconductor themed stocks, but cooling labour markets, expectations of economic slowdown, and uncertainty in speed of monetary easing from the Federal Reserve created a complex environment for investors heading into 2025. A strong performance from the Magnificent Seven could bolster confidence in the tech sector and support continued market momentum; however, any disappointments might highlight vulnerabilities in a market heavily dominated by these few major contributors. While the mega caps may continue deliver above-trend earnings growth and price performance, it is prudent to maintain a well diversified portfolio to lower concentration risk.

BoC rate cuts, U.S. - Canada yield spreads

In October 2024, the divergence between Canadian and U.S. interest rates became increasingly pronounced, with the Bank of Canada cutting its key lending rate to 3.75% while the U.S. Fed funds rate is currently at 5.0% after the aggressive 50bps cut, resulting in a notable 125 basis point spread. This gap is significant, outside of historical norm where a spread of around 100 basis points has typically been considered the "comfort zone." The last time the difference was so wide was during periods of economic stress or significant policy divergence, such as in the 1990s when it reached 250 basis points due to differing economic conditions in the two countries.

The implications of this widening spread are multifaceted, as a lower Canadian rate compared to the U.S. can lead to a depreciation of the Canadian dollar, which already fell sharply against the U.S. dollar during October. While U.S. GDP growth remains robust, Canadian growth has lagged, and therefore the gap in the path of rate cuts between the two countries may widen further. If Bank of Canada cuts rates more aggressively than the U.S., it is possible that the Canadian dollar may depreciate further against the U.S. dollar. The water in data collection is additionally muddied by disruptions caused by hurricanes Helene and Milton and a dockworkers' strike, adding noise to the latest U.S. labour market and economic growth data. As investors adjust their expectations for monetary policy and economic performance, this significant spread between Canadian and U.S. rates may continue to influence currency valuations and investment strategies heading into 2025.

Source: Bloomberg, NEI Investments

Legal

Aviso Wealth Inc. (“Aviso Wealth”) is the parent company of Credential Qtrade Securities Inc. (“CQSI”), Credential Asset Management (“CAM”), Qtrade Asset Management (“QAM”) and Northwest & Ethical Investments L.P. (“NEI”). NEI Investments is a registered trademark of NEI. Any use by CQSI, CAM, QAM or NEI of an Aviso Wealth trade name or trademark is made with the consent and/or license of Aviso Wealth. Aviso Wealth is a wholly-owned subsidiary of Aviso Wealth Limited Partnership, which in turn is owned 50% by Desjardins Financial Holdings Inc. and 50% by a limited partnership owned by the five Provincial Credit Union Centrals and the CUMIS Group Limited.

This material is for informational and educational purposes and it is not intended to provide specific advice including, without limitation, investment, financial, tax or similar matters. This document is published by CQSI, CAM and QAM and unless indicated otherwise, all views expressed in this document are those of CQSI, CAM and QAM. The views expressed herein are subject to change without notice as markets change over time. Views expressed regarding a particular industry or market sector should not be considered an indication of trading intent of any funds managed by NEI Investments. Forward-looking statements are not guaranteed of future performance and risks and uncertainties often cause actual results to differ materially from forward-looking information or expectations. Do not place undue reliance on forward-looking information. Mutual funds are offered through Credential Asset Management Inc. Mutual funds and other securities are offered through Credential Qtrade Securities Inc. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Unless otherwise stated, mutual fund securities and cash balances are not insured nor guaranteed, their values change frequently and past performance may not be repeated.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance, analysis, forecast or prediction. The MSSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to computing, computing or creating any MCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.