March 2025 Monthly Market Insights

March 2025 Monthly Market Insights

Data and opinions as of February 28, 2025

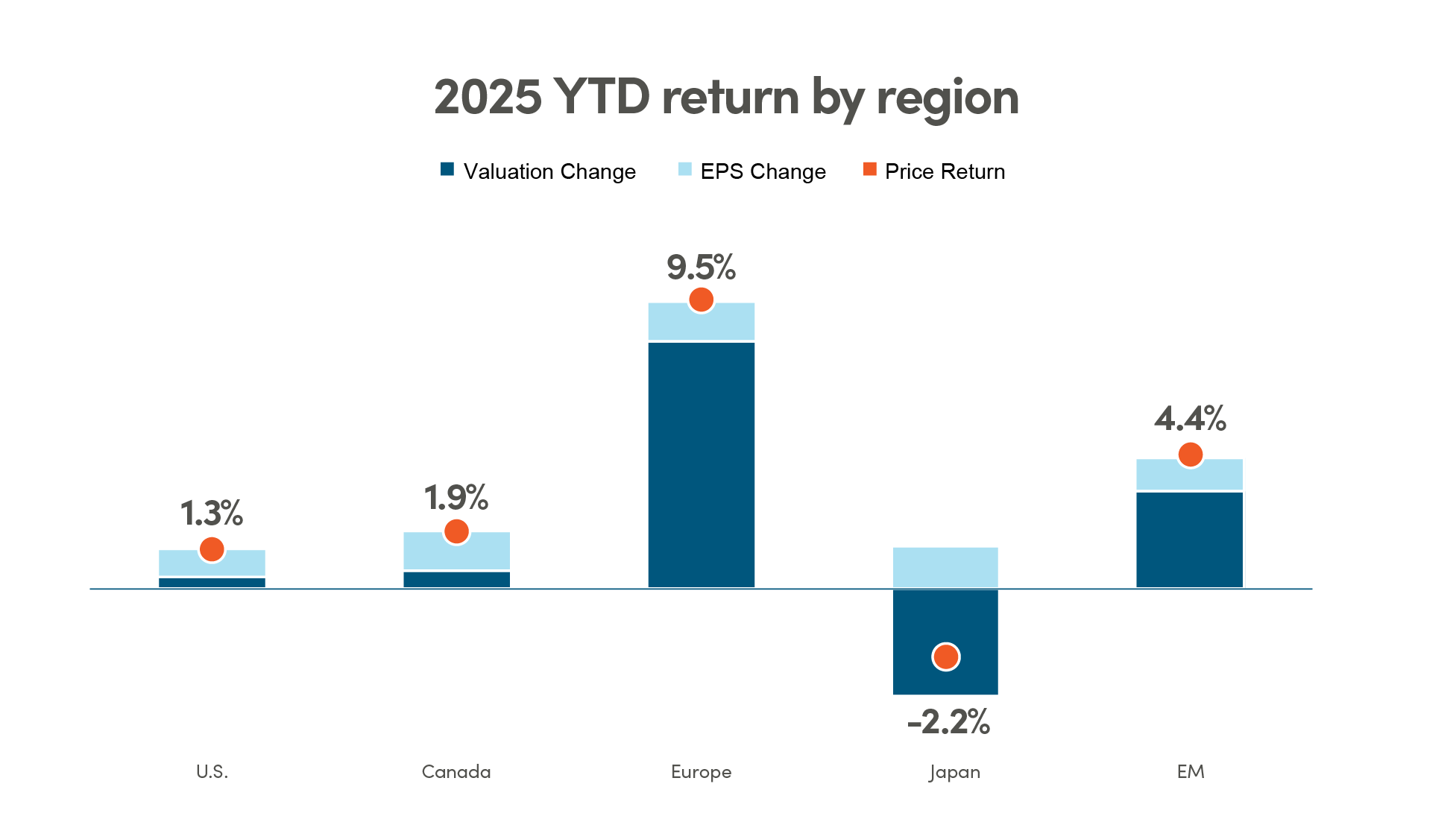

U.S. policy uncertainties, Canada’s resilience, & Europe’s growth

February 2025 was marked by heightened uncertainty in the U.S., with disruptive and protectionist policies fueling investor concerns of their impact on growth and inflation, amidst strong corporate earnings season. The new U.S. administration also stoked fear in Canada through tariff threats, but Canadian markets remained rather stable. Investors believe Canada can be resilient with the Bank of Canada’s (BoC) ability and the federal government’s willingness to provide support through policy flexibility, and a strong financial system. Meanwhile, European markets’ outperformance stood out, supported by earnings strength, monetary easing prospects, and strategic trade advantages to withstand U.S. tariffs. Investors sought diversification, rotating to European equities that offer growth at more reasonable valuations, and Canadian markets amid global uncertainty. Mega cap companies lost ground and underperformed the rest of the U.S. market, Tesla fell the most, by -27.6% in February.

NEI perspectives

U.S. policy uncertainty: Increasing fiscal and monetary policy uncertainty in the U.S. has led to heightened market volatility, with investors closely watching economic data for clarity. Bottom line: Policy uncertainty is likely to keep markets reactive, with potential implications for reduced economic growth and heightened risk sentiment.

Canada’s resilience: Despite global headwinds, Canada’s economy remains relatively stable, supported by a flexible monetary policy stance, a strong banking sector, and a weaker currency boosting exports. Bottom line: Canada’s economic fundamentals continue to provide stability, even as external pressures evolve.

Europe’s strength: European markets have benefited from strong corporate earnings, improving trade conditions, and expectations of central bank easing, with key sectors like luxury goods and industrials showing resilience. Bottom line: Europe’s relative economic strength and corporate performance suggest a more constructive outlook compared to other regions.

‒ NEI Asset Allocation team

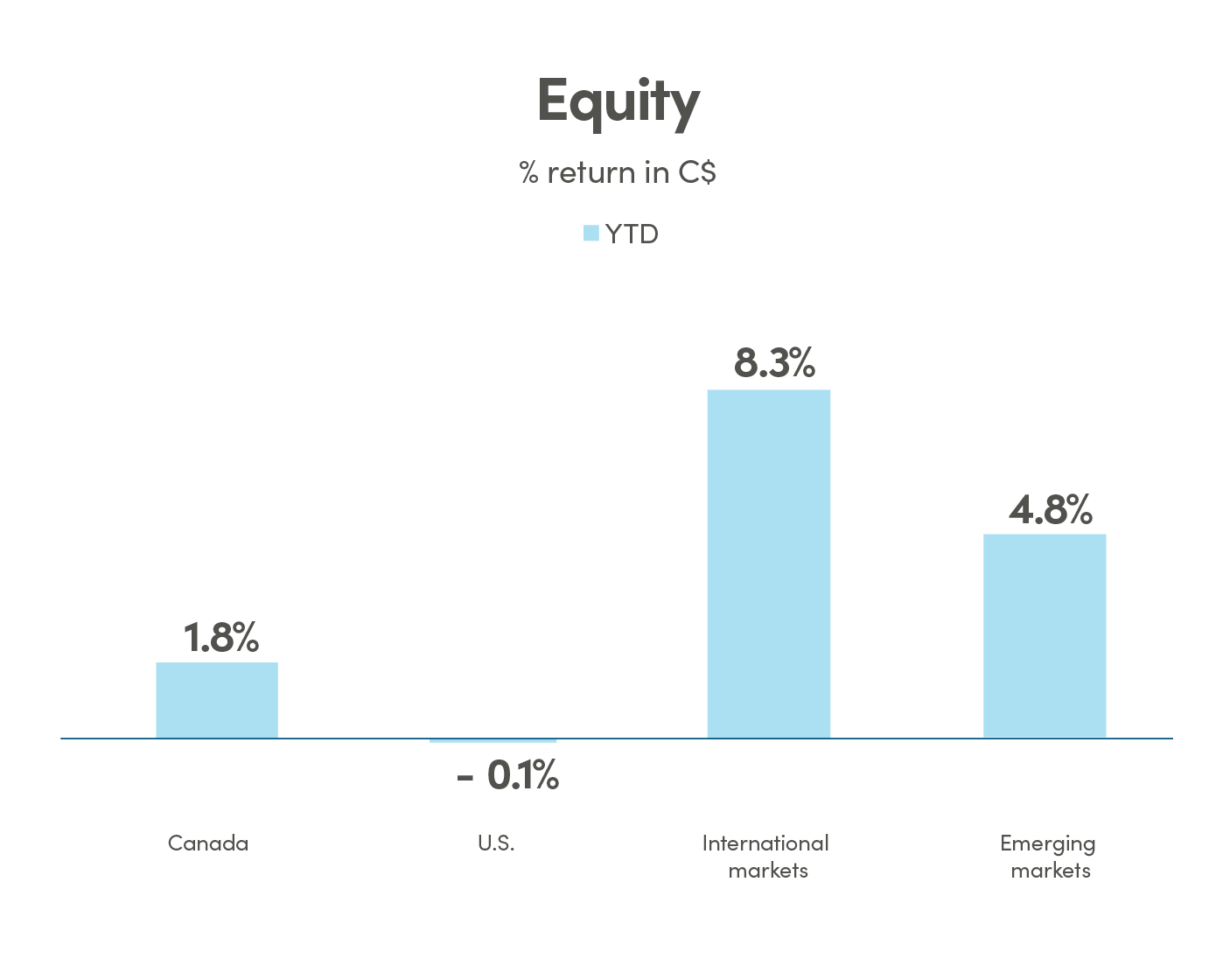

Canada: MSCI Canada; U.S.: MSCI USA International: MSCI EAFE; Emerging markets: MSCI Emerging Markets Index TR.

Source: Morningstar Direct

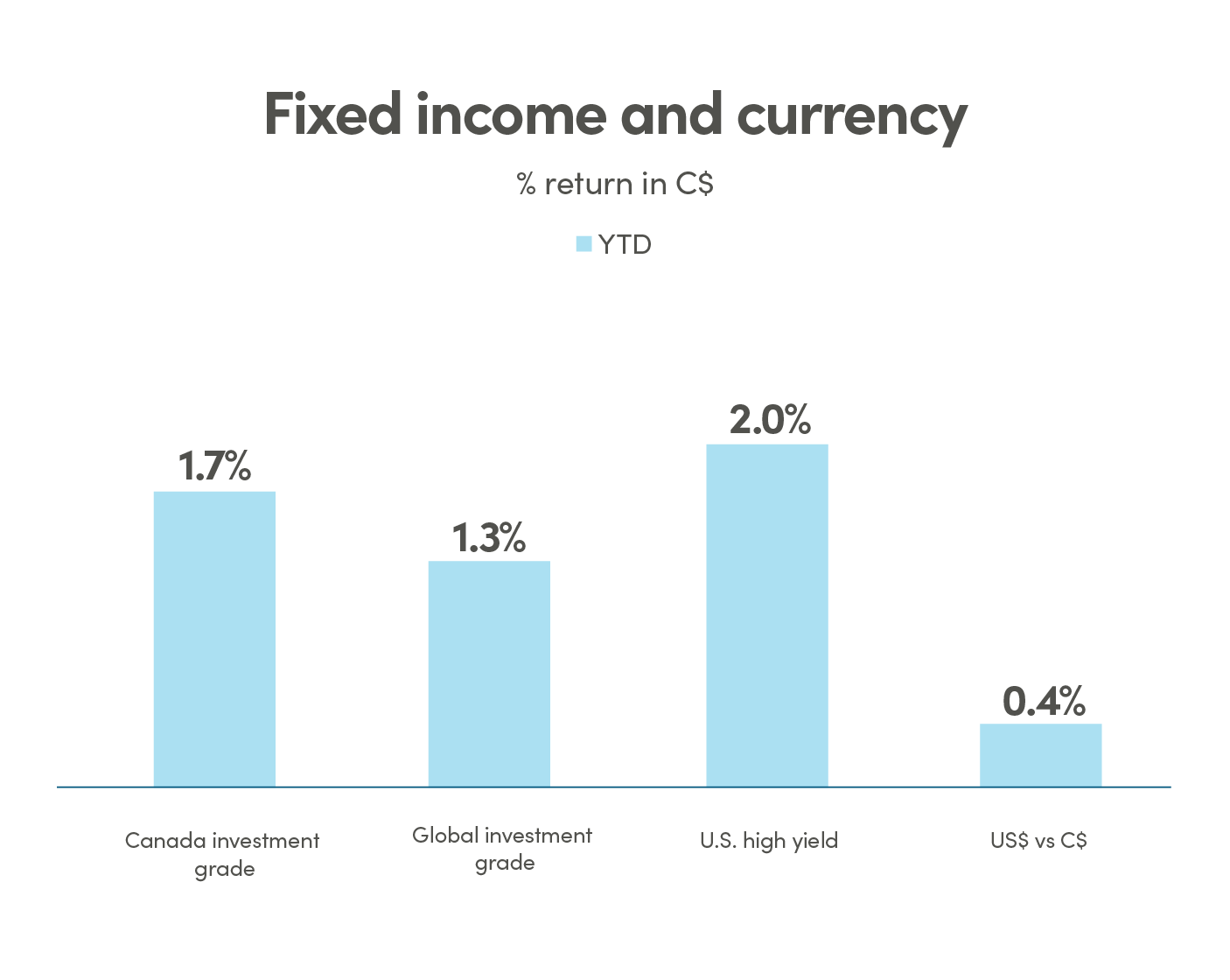

Canada investment grade: Bloomberg Barclays Canada Aggregate; Global investment grade: Bloomberg Barclays Global Aggregate; U.S. high yield: Bloomberg Barclays U.S. High Yield Index.

Source: Morningstar Direct

U.S. policy uncertainty weighs on markets

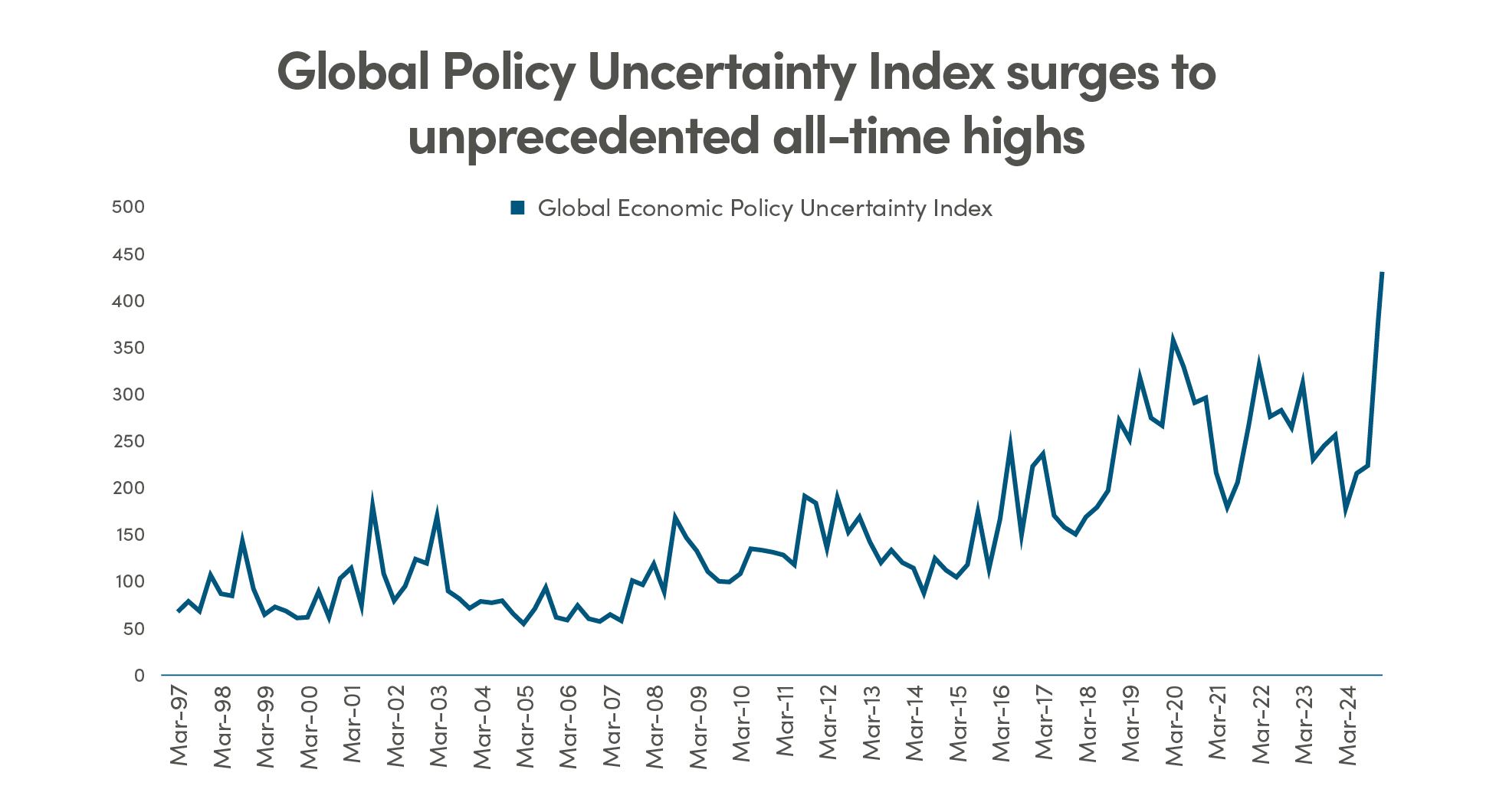

U.S. markets faced increasing volatility in February as investors were concerned about the impact of disruptive policies on growth and inflation. Areas that surged initially upon Trump’s election win reversed course, with cryptocurrency, Tesla, and the S&P 500 Index turning negative on year-to-date basis. Weaker-than-expected economic data also weighed on the market, as the Economic Surprise Index plummeted into the negative region, consumer confidence dropped significantly, retail sales disappointed, and business investment stalled. Additionally, the Department of Government Efficiency (DOGE), implemented massive firings of federal employees that added further strain to labour market expectations. The U.S. Policy Uncertainty Index surged, underscoring growing concerns over legislative gridlock and uncertainty around federal spending priorities. The administration issued numerous tariff threats to its closest trade partners, raising concerns on the inflationary risk while hurting growth. The Federal Reserve remained divided, with some officials pushing for rate cuts to counteract slowing growth, while others remain cautious due to persistent inflation risks.

Compounding these concerns were debates over potential deregulations in key industries, including technology and energy. This created additional market anxiety. Investors grappled with mixed signals from policymakers, making it increasingly difficult to assess the near-term economic outlook.

Bottom line: Rising policy uncertainty, weakening economic data, and fiscal austerity measures could prove detrimental to growth and investor sentiment. This is especially worrying at a time when U.S. valuations remain near historical highs. Investors need to remain vigilant in diversifying to more reasonable segments of the market, and to other regions with growth and more reasonable valuations such as Europe and Canada.

Source: Bloomberg

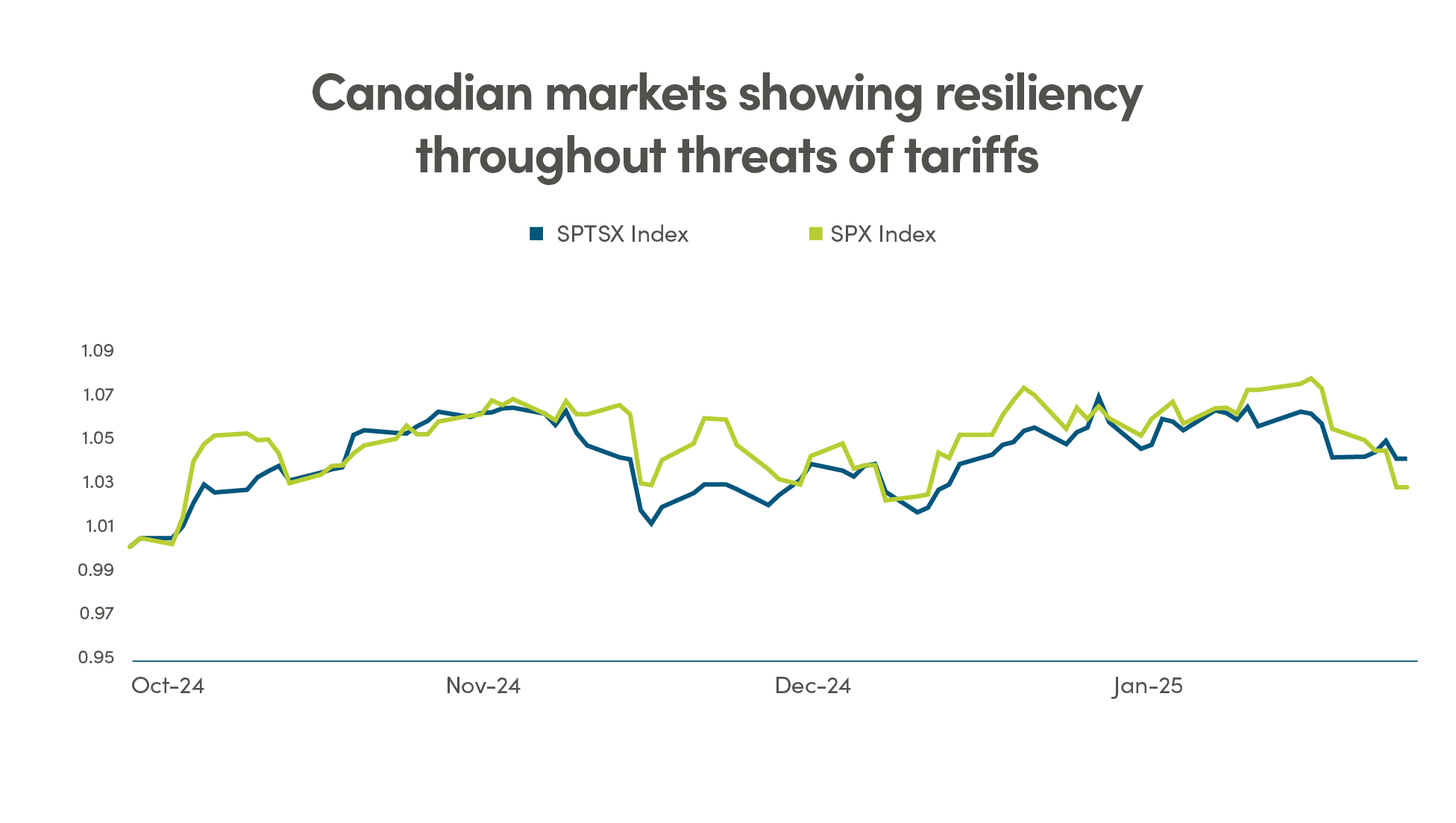

Canada’s resilience amid looming tariffs and global uncertainty

Canada reported surprising strong GDP growth for Q4 of 2024 on the back of strong consumption, and residential and business investments. The GDP per capita growth was the strongest in seven quarters, as rate cuts were successful in stimulating the economy thus far. The imposition of 25% tariffs poses a serious threat to the Canadian economy, and may plunge it into a mild recession if the tariffs are not lifted. However, the TSX would likely be more resilient and less impacted by tariffs than the Canadian economy. Earnings growth in Canadian companies are recovering well in the coming quarters. The Canadian market’s heavy exposure to energy, materials, and financials also makes it less sensitive to short-term trade disruptions, helpful in weathering the tariff storm. The banking sector is well capitalized and provisioned, and companies with foreign currency revenues would also benefit from a weakening loonie. Additionally, Canada has one of the lowest fiscal deficits in the G7, giving the federal government the ability to provide targeted fiscal support to affected industries, or more directly to consumers. Concerns about mortgage renewals, which had previously been a headwind for Canadian consumers, appear to be overstated. Rising household savings rates and stable employment levels have provided a financial buffer, alleviating fears of widespread financial distress.

The BoC is still expected to cut rates two more times this year, but has room to cut more aggressively to support growth if needed. However, this would further widen the rates gap between the two countries, resulting in further weakening of the loonie.

Bottom line: With ample dry powder in fiscal and monetary policy, and improving export conditions with a weakened currency, Canada’s economy has the ability to deal with the tariff threats. The impact on the TSX might even be smaller, since the heavyweights like energy, materials, and financials are less impacted by tariffs. Canadian fixed income and equities remain attractive with prospects of two more rate cuts, strengthening earnings growth and reasonable valuations.

Source: Bloomberg

Europe’s momentum: supported by strong fundamentals

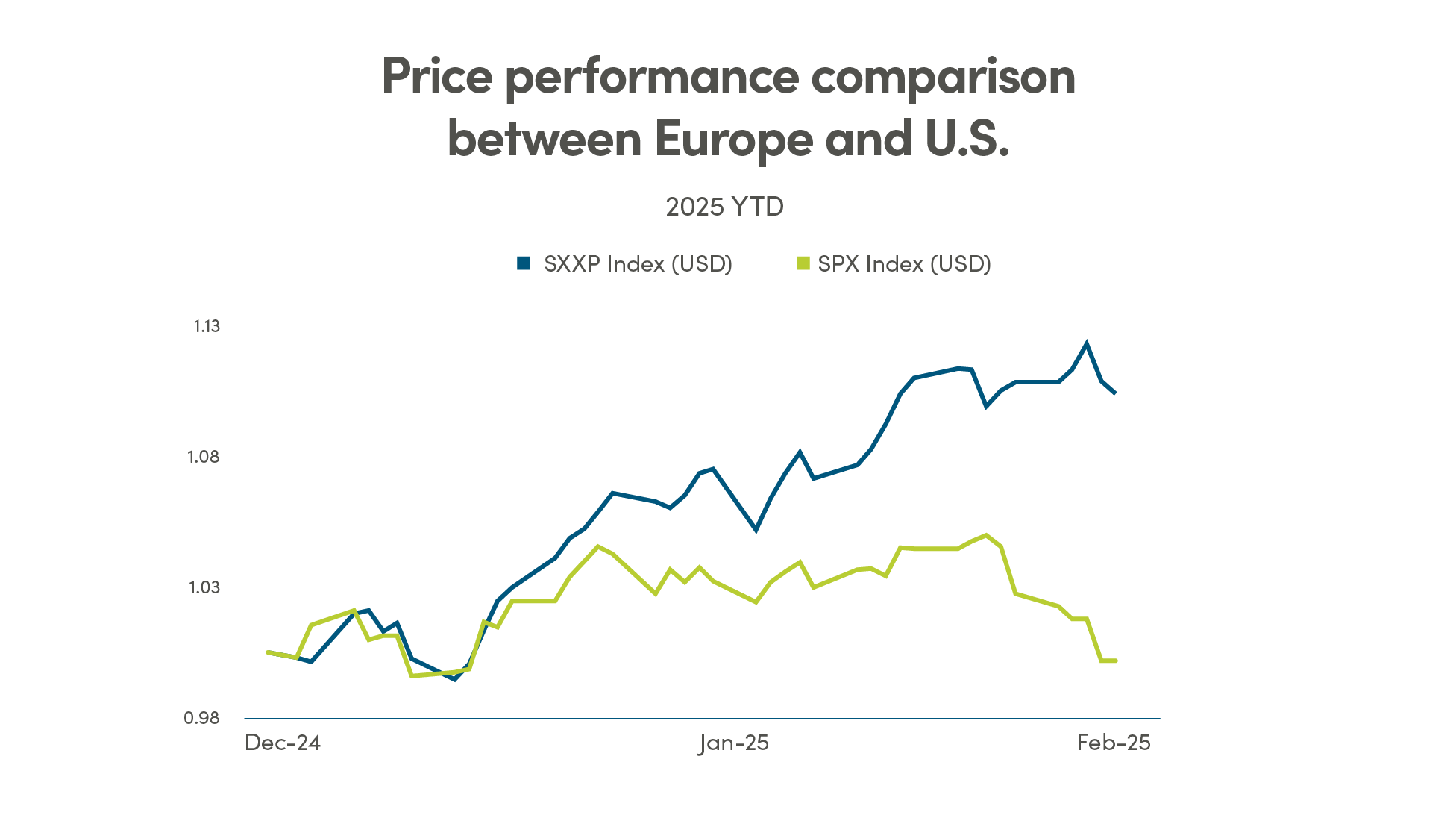

European markets continued to outperform North American equity markets in February, bolstered by strong corporate earnings, favorable trade agreements, and resilient consumer demand. The U.S.-Ukraine minerals agreement provided a significant boost to industrial and materials stocks, particularly in construction, infrastructure, and semiconductor supply chains. Leading European firms, including luxury and consumer goods companies such as LVMH and Richemont, also posted better-than-expected earnings, reinforcing optimism about the region’s economic trajectory.

European Central Bank (ECB) policy expectations also played a key role in driving investor sentiment. With inflation moderating, the ECB is expected to continue to ease rates later in 2025, which could further support rate-sensitive sectors such as real estate and utilities. Additionally, European equity valuations remain attractive relative to U.S. markets, as earnings growth continues in several sectors. This valuation gap has drawn increased interest from global investors seeking opportunities outside the U.S.

European stocks surged in 2025, driven by improved sentiment on growth

Source: Bloomberg.

Beyond Europe, emerging markets are also showing signs of stabilization, particularly in China. Lower-than-expected U.S. tariffs and advancements in artificial intelligence have fueled optimism in China’s technology sector, which has been a key driver of recent gains in Asian equities. While geopolitical concerns and secular challenges persist, selective opportunities in China’s IT and consumer discretionary sectors are gaining investor attention.

Bottom line: In a highly uncertain regime which will reward diversification, Europe offers a compelling investment destination, supported by strong earnings, central bank easing prospects, and favorable valuations. Selective opportunities are also available in emerging markets with favorable valuations and growth.

Data and opinions as of February 28, 2025.

Legal

Aviso Wealth Inc. (“Aviso”) is the parent company of Aviso Financial Inc. (“AFI”) and Northwest & Ethical Investments L.P. (“NEI”). Aviso and Aviso Wealth are registered trademarks owned by Aviso Wealth Inc. NEI Investments is a registered trademark of NEI. Any use by AFI or NEI of an Aviso trade name or trademark is made with the consent and/or license of Aviso Wealth Inc. Aviso is a wholly-owned subsidiary of Aviso Wealth LP, which in turn is owned 50% by Desjardins Financial Holding Inc. and 50% by a limited partnership owned by the five Provincial Credit Union Centrals and The CUMIS Group Limited.

This material is for informational and educational purposes and it is not intended to provide specific advice including, without limitation, investment, financial, tax or similar matters. This document is published by AFI and unless indicated otherwise, all views expressed in this document are those of AFI. The views expressed herein are subject to change without notice as markets change over time. Views expressed regarding a particular industry or market sector should not be considered an indication of trading intent of any funds managed by NEI Investments. Forward-looking statements are not guaranteed of future performance and risks and uncertainties often cause actual results to differ materially from forward-looking information or expectations. Do not place undue reliance on forward-looking information. Mutual funds and other securities are offered through Aviso Financial Inc. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Unless otherwise stated, mutual fund securities and cash balances are not insured nor guaranteed, their values change frequently and past performance may not be repeated.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance, analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to computing, computing or creating any MCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

©2025 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar Research Services LLC, Morningstar, Inc. and/or their content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar Research Services, Morningstar nor their content providers are responsible for any damages or losses arising from any use of this information. Access to or use of the information contained herein does not establish an advisory or fiduciary relationship with Morningstar Research Services, Morningstar, Inc. or their content providers. Past performance is no guarantee of future results.