December 2024 Monthly Market Insights

Data and opinions as of November 30, 2024

NEI perspectives

Results of the U.S. election enhanced market optimism since Nov 6, which was further fueled by robust economic data on consumer spending and job growth. Financial stocks benefited from expectations of regulatory rollbacks, while clean energy stocks struggled on concerns over policy reversals. Bottom line: the election has buoyed positive sentiment for markets.

President-elect Donald Trump plans to impose a 25% tariff on all imports from Canada and Mexico, raising concerns about economic disruption and retaliatory measures. While Canadian industries may face challenges, analysts expect impact to be manageable. Bottom line: tariffs could heavily strain U.S.-Canada trade relations.

The yield curve has significantly flattened following the U.S. election, driven by consensus that Trump’s policies on tax cuts, tariffs and immigration could be inflationary. While long-term inflation forecasts remained stable, bullish sentiment on risk assets pushed long-term yields lower by more than short-term yields. Bottom line: the election results generated speculation of easy regulatory conditions and corporate tax cuts, leading to a positive growth outlook, but potential inflation risks and policy shifts may create market volatility heading into 2025.

-NEI

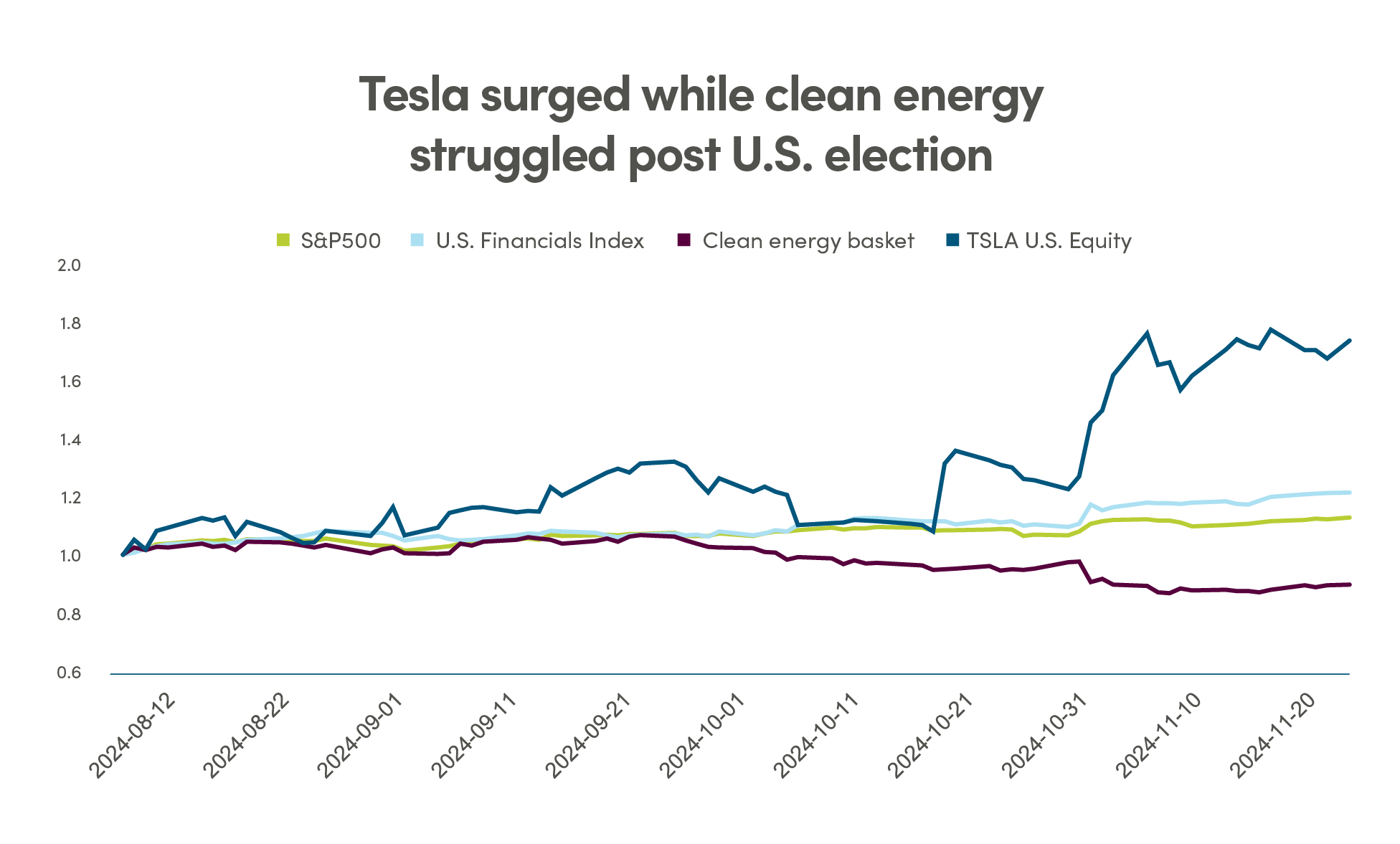

U.S. markets make new highs on Trump’s win

Speculations about the impact on Donald Trump’s return to the White House has dominated headlines and markets. Market sentiment has generally been positive, further supported by the latest economic data showing strong consumer spending and job growth. Financial stocks moved higher, while clean energy stocks faced challenges due to policy concerns. President-elect Trump’s plan to impose a 25% tariff on imports from Canada and Mexico raised worries about serious economic disruption. Bottom line: the election fosters a positive market outlook, but trade tensions and policy shifts could create volatilities ahead.

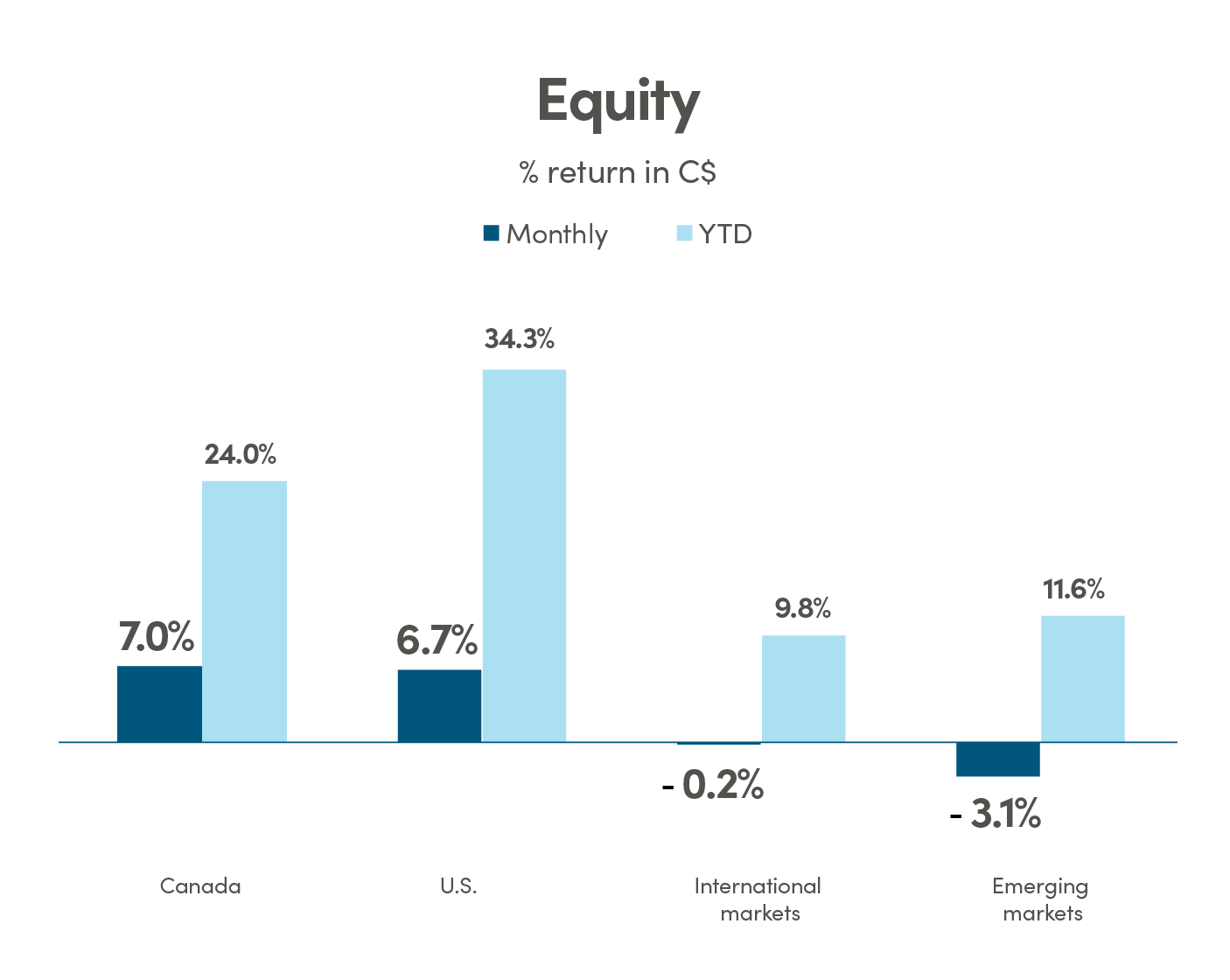

Canada: MSCI Canada; U.S.: MSCI USA International: MSCI EAFE; Emerging markets: MSCI Emerging Markets Index TR.

Source: Morningstar Direct

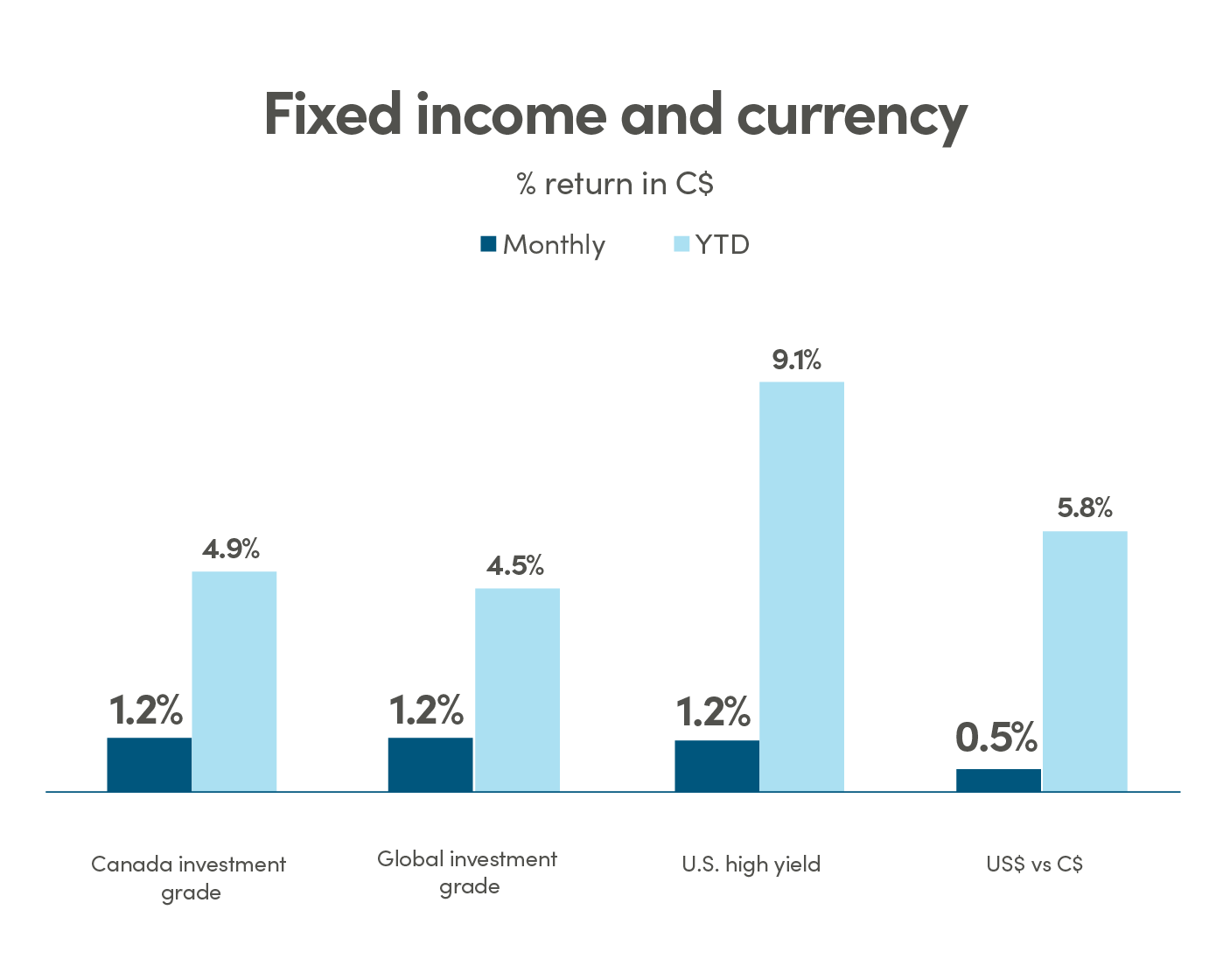

Canada Aggregate: Bloomberg Barclays Canada Aggregate; Global Aggregate: Bloomberg Barclays Global Aggregate; U.S. High Yield: Bloomberg Barclays U.S. High Yield Index.

Source: Morningstar Direct

U.S. election’s impact on markets

The U.S. election has significantly influenced market dynamics across various asset classes, but the overall macroeconomic climate remains generally positive, with no immediate signs of weakness. Robust consumer spending, stable job growth, and resilient corporate earnings have contributed to an optimistic outlook for the economy. Investors are increasingly adopting a more bullish stance on equities as they look ahead to 2025 despite elevated valuations, believing that favourable economic conditions will continue to support market upside. Following the election results, markets reacted swiftly. Equities broadly surged as investors positioned themselves for potentially stronger economic growth from broad-based corporate and personal tax cuts. However, certain sectors experienced more pronounced reactions based on their perceived alignment with the incoming administration's policies, leading to mixed performance across segments.

Focusing on specific sectors, clean energy stocks faced significant headwinds in the wake of the election results. Anticipation of a Trump-led administration raised concerns about potential rollbacks of supportive clean energy policies, which contributed to a decline in renewable energy equities. Conversely, financial stocks reacted positively as investors speculated on regulatory rollbacks and interest rate hikes that could enhance profitability.

Tesla (TSLA), despite being a bellwether for the clean energy movement, surged by 40% since the election from Elon Musk’s alignment with Trump. It remained a focal point for investors betting on long-term growth in electric vehicles and sustainable technologies. Overall, while clean energy faced immediate challenges post-election, financial stocks capitalized on optimism around economic recovery, highlighting the divergent paths taken by different sectors.

Source: Bloomberg

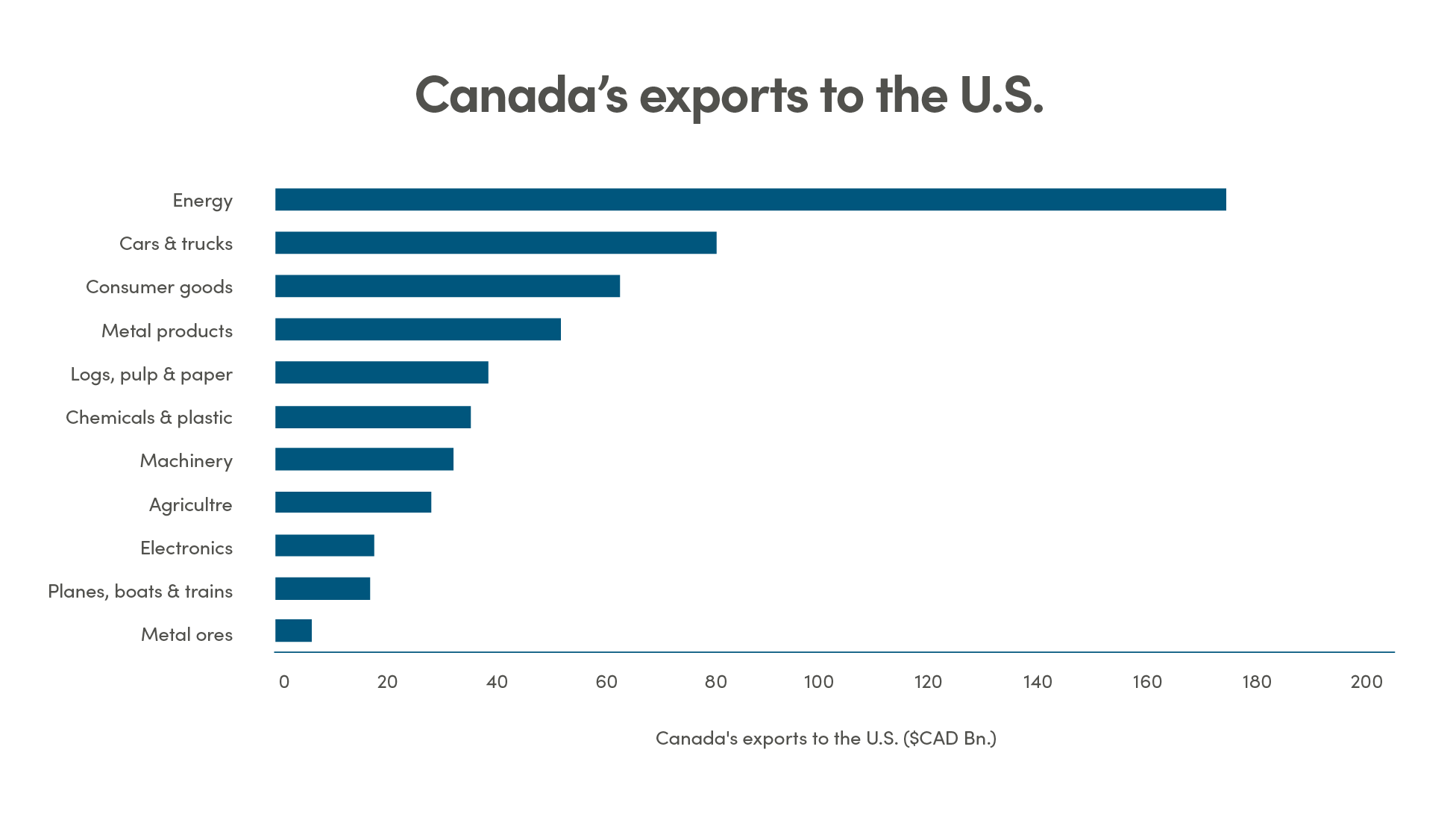

Implications of Trump tariffs for Canada

President-elect Donald Trump has announced plans to impose a 25% tariff on all imports from Canada and Mexico, effective immediately upon his inauguration. This decision is framed as a response to the perceived failure of these countries to address issues related to illegal immigration and drug trafficking. While the initial discussion centred around a 10% tariff, the escalation to 25% has raised concerns about its potential economic impact. Analysts suggest that these tariffs may serve as a negotiation tactic rather than an outright intention, but if implemented, they could disrupt established trade agreements like the United States-Mexico-Canada Agreement (USMCA) and lead to retaliatory measures from affected countries.

The implications for Canada could be substantial, given the deep economic ties between the U.S. and Canada, with approximately $3.6 billion in goods crossing the border daily. Exports make up about a third of Canada’s economic activity and over 75% of exports go to the U.S. Canadian industries that rely heavily on cross-border supply chains, such as automotive and energy sectors, may face increased costs and disruptions.

Potential tariffs pose a negative impact for the Canadian economy, which is already operating below its potential growth rates. Additionally, Trump’s support of traditional energy production may lower the price of oil, further dragging down the Canadian economy. The balance of risk points to lower Bank of Canada rates. Typically, Bank of Canada (BoC) rates are within 1% of U.S. Federal Reserve policy rates. However, the widening gap between the two countries’ growth rates may push the BoC rates beyond the typical range, putting even more downward pressure on the Canadian dollar.

Source: Bloomberg

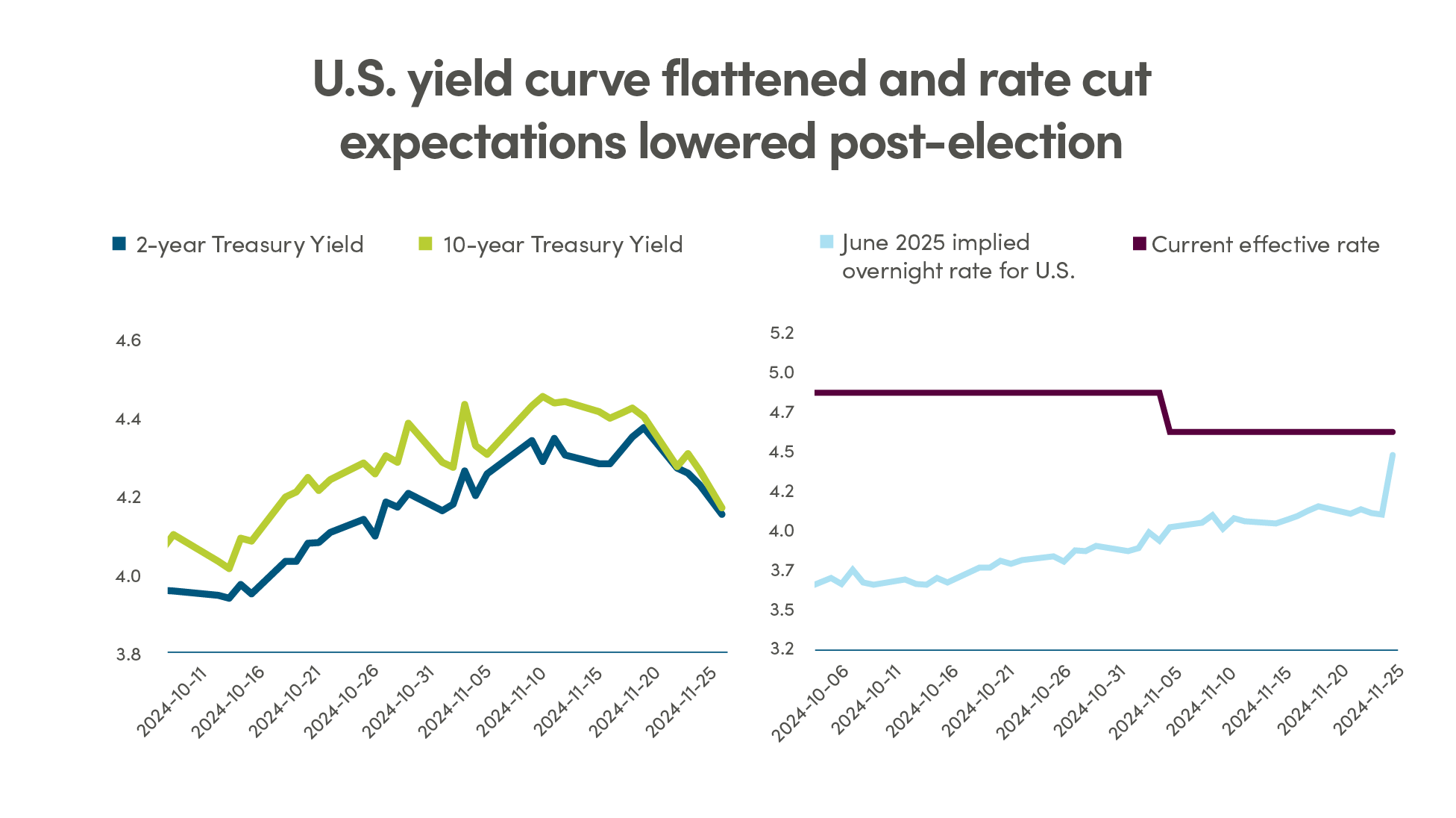

Rate cuts expectations evaporated due to inflationary policies

The U.S. presidential election has swiftly influenced the yield curve, altering the path of rate cut expectations. Following the election, the yield curve flattened, with 10-year Treasury yields falling sharply, more so than the 2-year bond yields. Bond investors anticipate stronger domestic economic growth, due to the lowering of personal and corporate taxes proposed by President-elect Trump, the imposition of tariffs on imports, reduced immigration, and supportive policies in the energy sector. With the inflationary net impact of these policies, the bond markets have effectively eliminated expectations of three rate cuts by June 2025, maintaining rates at their current levels.

Source: Bloomberg

For Canada and its markets, the implications of these developments are multifaceted. The potential for increased U.S. government debt and higher interest rates could lead to a weaker Canadian dollar, which may enhance export competitiveness but also raise inflationary concerns domestically. Canadian markets, particularly those heavily reliant on cross-border trade with the U.S., could face challenges if tariffs are imposed or if U.S. economic policies lead to increased costs. However, analysts believe that while some sectors may be affected by these tariff threats, the overall impact on the Canadian economy will be manageable. As Canada navigates its economic relationship with a new U.S. administration, maintaining strong trade ties will be crucial for mitigating any adverse effects stemming from changes in U.S. fiscal and monetary policy leading into 2025.

Legal

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus and/or Fund Facts before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. ©2024 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar Research Services LLC, Morningstar, Inc. and/or their content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar Research Services, Morningstar nor their content providers are responsible for any damages or losses arising from any use of this information. Access to or use of the information contained herein does not establish an advisory or fiduciary relationship with Morningstar Research Services, Morningstar, Inc. or their content providers. Past performance is no guarantee of future results.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance, analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to computing, computing or creating any MCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

NEI Investments is a registered trademark of Northwest & Ethical Investments L.P. (“NEI LP”). Northwest & Ethical Investments Inc. is the general partner of NEI LP and a wholly-owned subsidiary of Aviso Wealth Inc. (“Aviso”). Aviso is the sole limited partner of NEI LP. Aviso is a wholly-owned subsidiary of Aviso Wealth LP, which in turn is owned 50% by Desjardins Financial Holding Inc. and 50% by a limited partnership owned by the five Provincial Credit Union Centrals and The CUMIS Group Limited.