April 2024 Monthly Market Insights

Data and opinions as of March 31, 2024

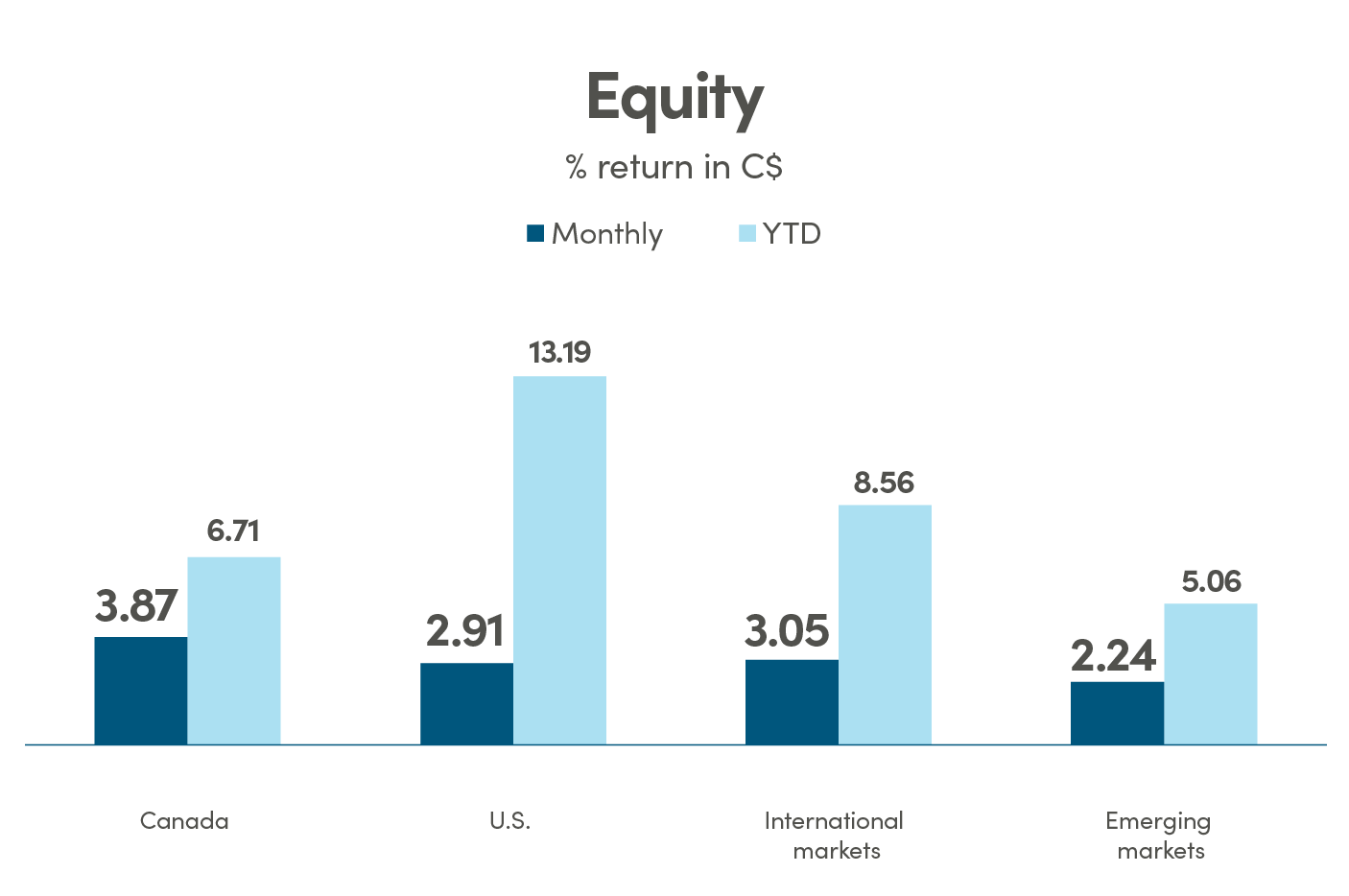

Unstoppable equity market rally on soft landing narrative

Resilient economic data throughout the first quarter supported the soft landing narrative and pushed equity markets around the world to new record highs. Global equities posted strong returns with the MSCI ACWI Index up 11.0% during the first quarter. In Canada, the TSX gained 6.6% and in the U.S., the S&P 500 rose 10.6%, driven once again by several of the mega-cap names which posted strong earnings growth. However, the best performing market of the quarter was Japan, up 13.9% for the quarter in Canadian dollar terms.

Many European indices reached new all-time highs in March. While they lagged the U.S. and Japan for the quarter, Europe was the top performing region in March. Investors are looking to mitigate the concentration risks in the U.S. market, while turning to Europe for its cheaper valuation and re-acceleration of earnings.

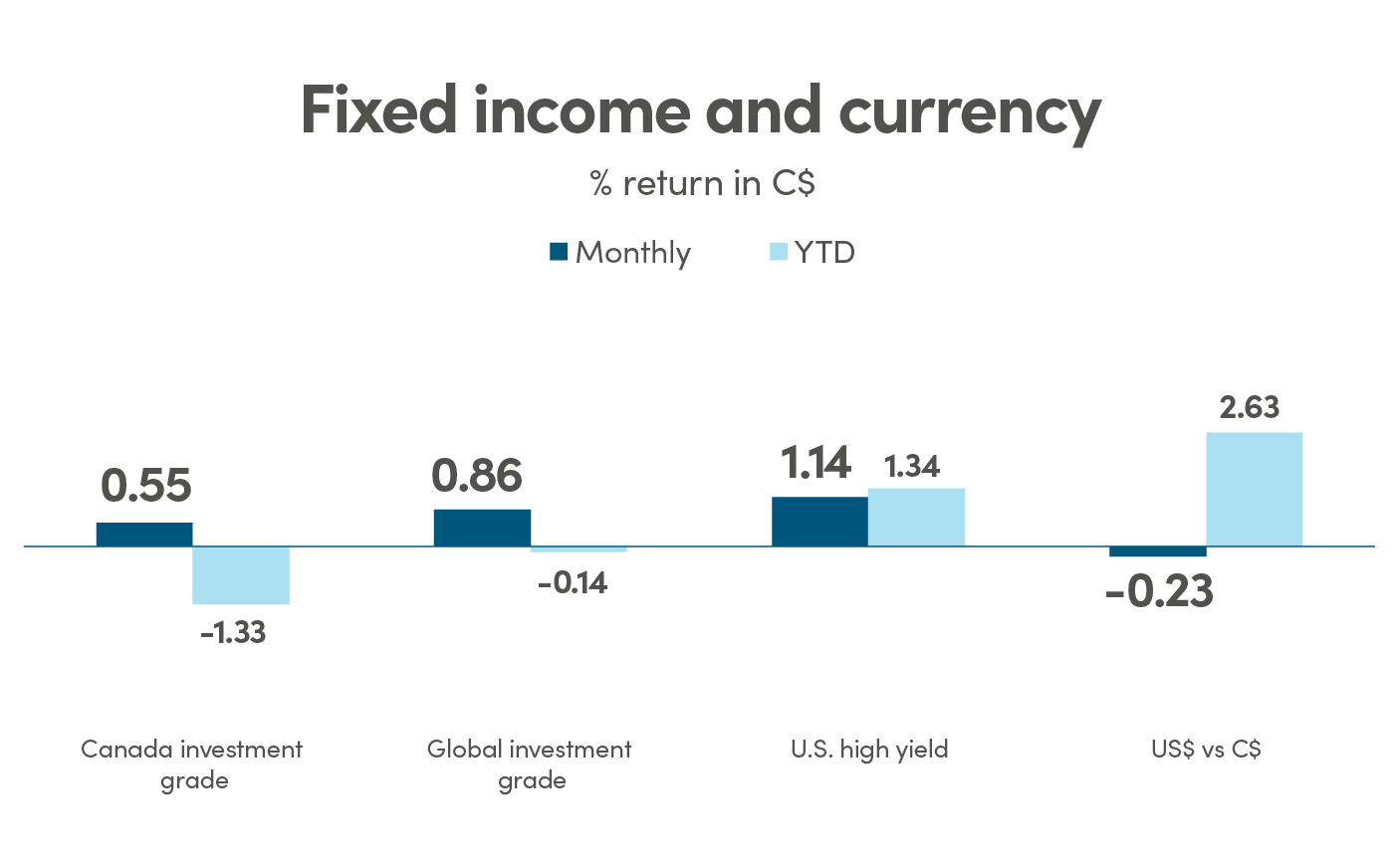

While equity investors welcomed strong economic data, it was a more challenging period for fixed income investors. Stickier inflation and resilience in economic activity have shifted market expectations of rate cuts and push yields higher. The FTSE Canadian Universe Bond Index was 1.2% lower and Global Aggregate Bond index fell -0.1% for the quarter.

The NEI perspective

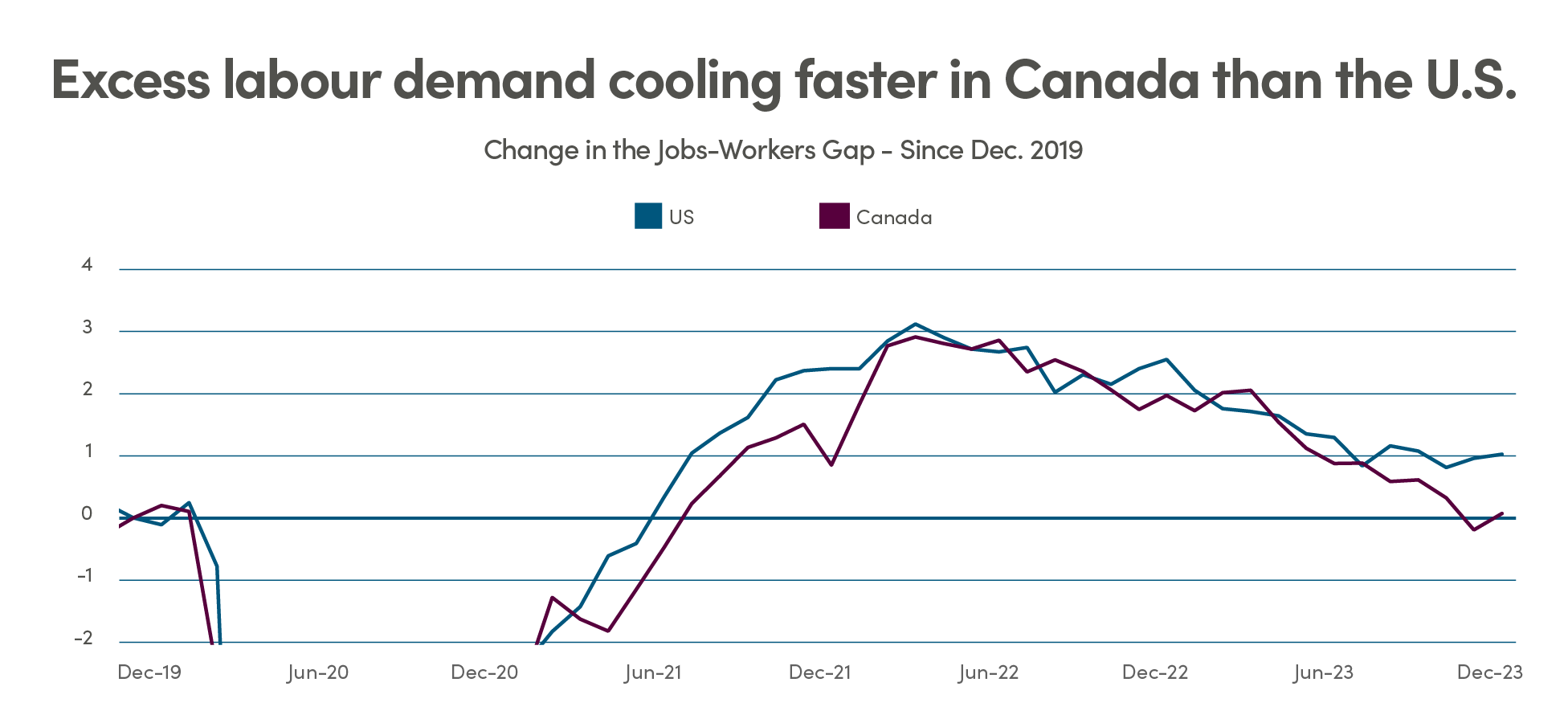

Labour market conditions are showing signs of cooling as the expansion of the labour force outpaces job creation. In the U.S., the number of job openings still exceeds the available labour supply, whereas in Canada, a rapid expansion of the labour force combined with slowing employment growth has resulted in an increase in unemployment.

The latest inflation numbers in Canada came in lower than expected, supporting the possibility of the Bank of Canada reducing interest rates soon. Many predicting this easing cycle could begin in June amid a weakening economy and cooling labour market.

60/40 portfolios have traditionally been effective in taking advantage of the stock and bond correlation which has mostly been negative since the turn of the century. However, the dramatic rise in inflation and interest rates in the past couple of years has created a more difficult environment for returns.

From NEI’s Monthly Market Monitor for March.

Canada: MSCI Canada; U.S.: MSCI USA; International markets: MSCI EAFE; Emerging markets: MSCI Emerging Markets. Source: Morningstar Direct

Canada investment grade: Bloomberg Barclays Canada Aggregate; Global investment grade: Bloomberg Barclays Global Aggregate; U.S. high yield: Bloomberg Barclays U.S. High Yield. Source: Morningstar Direct.

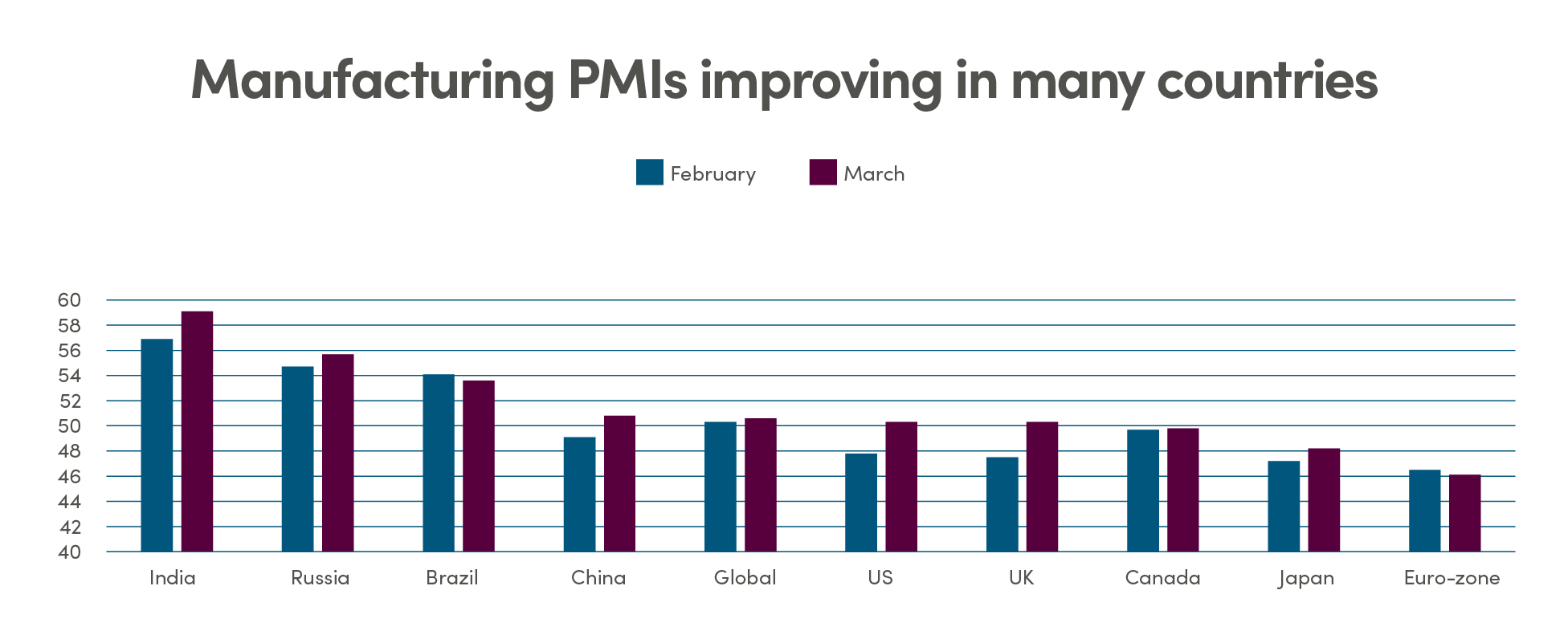

Continued Strength in economic activities

Global Manufacturing PMIs are showing signs of improvement, bucking the trend of contraction over the past year. U.K. is the latest to join the group of countries in expansionary territory (index level above 50). Although this is only one data point and both Europe and U.K.’s GDP growth are still below trend, this could be tentative indication of an inflection point.

Source: Bloomberg, NEI Investments

Labour market conditions are cooling, with labour force expansion outpacing growth in job creation. In the U.S., job openings continue to exceed labour supply, albeit at a lower rate, helping the unemployment rate to remain low at 3.8% in March. In Canada, however, employment growth has slowed in recent months while the labour force has been expanding rapidly, leading to a jump in the unemployment rate from 5.8% in February to 6.1% in March.

Source: Goldman Sachs, NEI Investments

Canada banks pause on stubborn inflation

In Canada, inflation data came in lower than expected with CPI at 2.8% vs. forecast of 3.1%, marking the weakest pace since June of last year and down from the prior month’s reading of 2.9%, helping the Bank of Canada’s case to pivot to cutting interest rates in the months ahead. The trend of easing inflation is leading many to predict the easing cycle to start in June as the economy weakens and the labour market cools.

Inflation continues to be a bumpy ride in the U.S., with core inflation coming in hotter than expected in February, making it two consecutive months of stronger than expected readings on core inflation. The Fed’s preferred measure of underlying inflation, the core PCE price index did moderate, rising by 0.3%, less than the 0.5% increase in February.

The Fed also held the rates unchanged for the fifth consecutive time in line with expectations as they wait for greater confidence on inflation before initiating rate cuts. With robust economic growth and a resilient labour market, investors may need to remain patient as they wait for the initial cut. The data has led Fed officials to reiterate that the central bank does not feel rushed to cut interest rates, with some economists warning that a rate cut in June may be a little too optimistic. Some strategists are even speculating there won’t be any cuts at all in 2024.

While most central banks in developed markets are contemplating rate cuts, the Bank of Japan hiked rates for the first time in 17 years and eliminated the negative interest rate regime to combat rising inflation. However, the bank's cautious remarks have had a negative impact on the Yen, as the dovish commentary and lack of clues on future moves indicated that this is not the start of a full-fledged tightening phase like the ones witnessed in the U.S. and Europe in recent years.

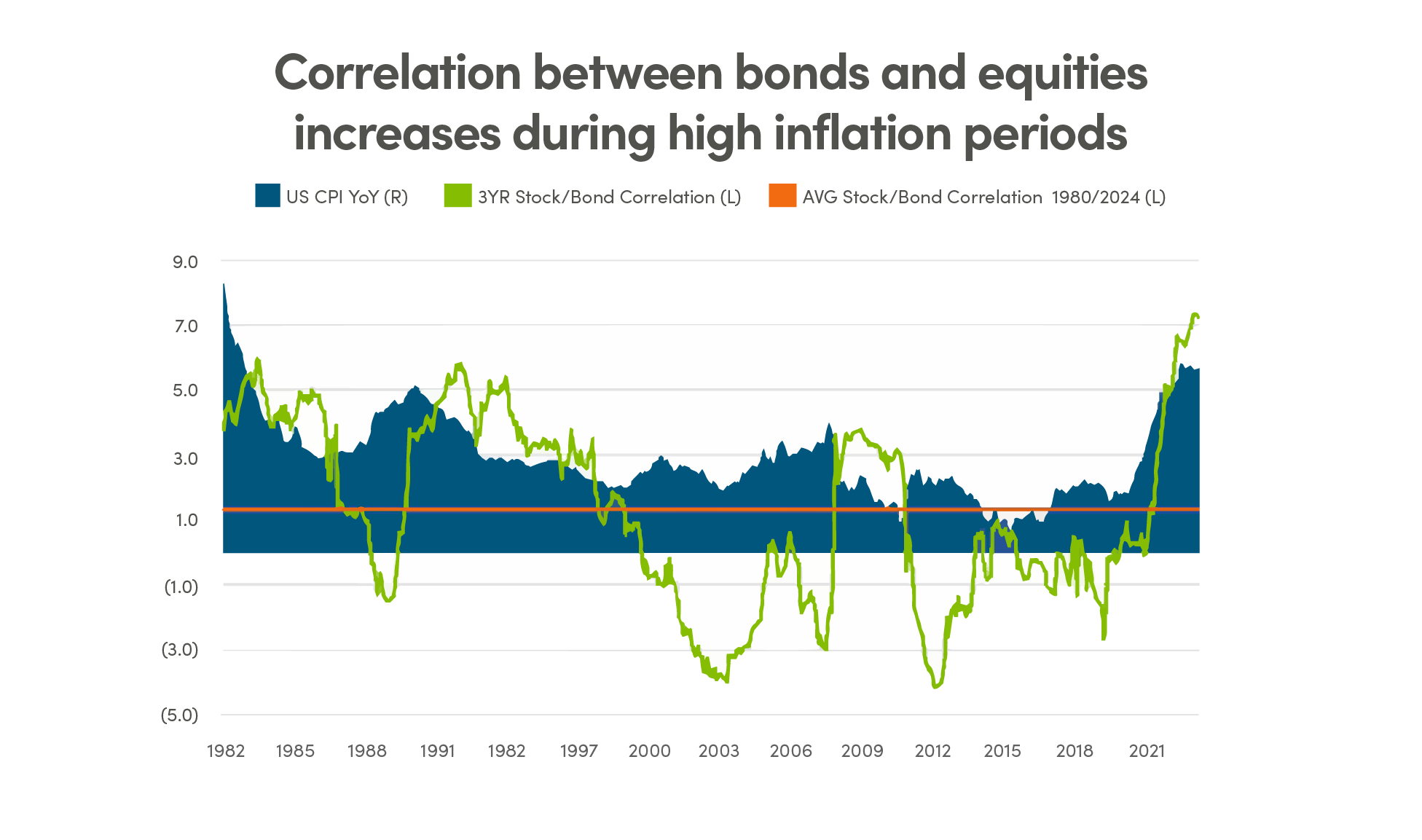

Going beyond the traditional 60/40

Traditional 60/40 portfolios have been effective in taking advantage of the stock and bond correlation which has mostly been negative since the turn of the century. The dramatic rise in inflation and interest rates in 2022 however, created a difficult environment on both stocks and bonds, hence returns in traditional 60/40 portfolios.

Source: Bloomberg, NEI Investments

In search of levers to enhance portfolio resilience, investors are increasingly looking for strategies that have different drivers of returns. Alternatives such as long-short equity strategies, real assets, or strategies with absolute return focus are well-suited as they complement traditional asset classes with alternative sources of return that provide portfolio diversification.

Bottomline: Investors should consider expanding their toolkit to utilize strategies with lower correlation to traditional stocks and bonds to help improve portfolio diversification, enhance returns, and protect against volatility. In the case of long-short equities strategy, the flexibility to capitalize on both rising and falling stock prices can be a valuable component of a diversified investment portfolio.

Legal

Aviso Wealth Inc. (“Aviso”) is the parent company of Aviso Financial Inc. (“AFI”) and Northwest & Ethical Investments L.P. (“NEI”). Aviso and Aviso Wealth are registered trademarks owned by Aviso Wealth Inc. NEI Investments is a registered trademark of NEI. Any use by AFI or NEI of an Aviso trade name or trademark is made with the consent and/or license of Aviso Wealth Inc. Aviso is a wholly-owned subsidiary of Aviso Wealth LP, which in turn is owned 50% by Desjardins Financial Holding Inc. and 50% by a limited partnership owned by the five Provincial Credit Union Centrals and The CUMIS Group Limited.

This material is for informational and educational purposes and it is not intended to provide specific advice including, without limitation, investment, financial, tax or similar matters. This document is published by AFI and unless indicated otherwise, all views expressed in this document are those of AFI. The views expressed herein are subject to change without notice as markets change over time. Views expressed regarding a particular industry or market sector should not be considered an indication of trading intent of any funds managed by NEI Investments. Forward-looking statements are not guaranteed of future performance and risks and uncertainties often cause actual results to differ materially from forward-looking information or expectations. Do not place undue reliance on forward-looking information. Mutual funds and other securities are offered through Aviso Financial Inc. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Unless otherwise stated, mutual fund securities and cash balances are not insured nor guaranteed, their values change frequently and past performance may not be repeated.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance, analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to computing, computing or creating any MCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.